While opting for any loan in India, lenders don’t ask for the borrowed amount at one go; rather, they divide the amount in monthly instalments for the repayment. These instalments are also known as EMI (Equated Monthly Instalments). The EMI comprises both principal and interest due to the lender. Let us understand the concept in detail so that you can plan the borrowings and repayments well before taking any loans and help to avoid any surprises.

What Is EMI?

The equated monthly instalment, or EMI as we call it in simple terms, comprises a fixed amount that is paid monthly over a fixed period of time, which is decided at the time of sanction of the loan. Each EMI consists of two components: an amount that is towards principal repayment, i.e., the borrowed amount, and another portion that goes towards interest charged by the lender on the principal amount.

Generally, the interest component is higher during the initial installments, which is due to interest being charged on the reducing balance. As the loan matures, the ratio of interest and principal payment reverses, making a larger amount getting adjusted towards the principal outstanding.

The EMI Calculation Formula

Banks and NBFCs in India use the reducing balance method to calculate EMI. The standard formula is:

EMI = [P × R × (1 + R)^N] ÷ [(1 + R)^N − 1]

Where:

- P = Principal loan amount (in ₹)

- R = Monthly interest rate = Annual interest rate ÷ 12 ÷ 100

- N = Loan tenure in months

This formula accounts for compound interest on the outstanding principal, which reduces with every payment — hence the name “reducing balance.”

Step-by-Step Example

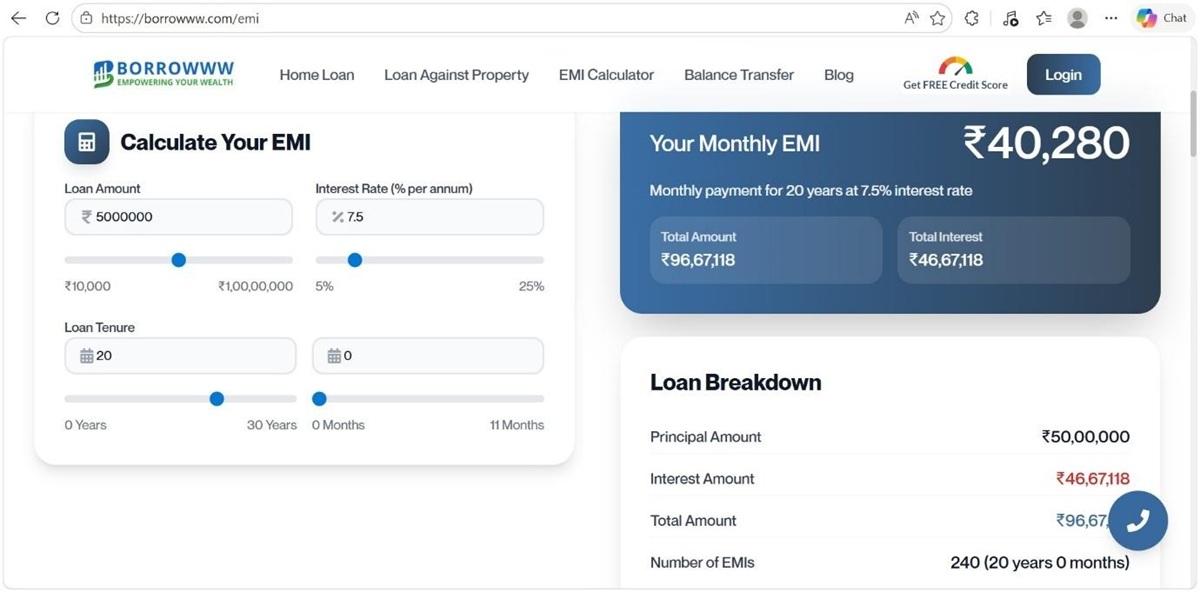

Let us understand this with the help of a simple example. For a home loan of ₹50,00,000 at an annual interest rate of 7.5% for 20 years (240 months).

Step 1 — Find the monthly rate (R): R = 7.5 ÷ 12 ÷ 100 = 0.00625

Step 2 — Calculate (1 + R)^N: (1 + 0.00625)^240 = 4.4650 (approx.)

Step 3 — Apply the formula: EMI = [30,00,000 × 0.00625 × 4.4650] ÷ [4.4650 − 1]

EMI ≈ ₹40,280 per month

Step 4 — Total amount paid over 20 years: ₹40,280 × 240 = ₹96,67,200

Step 5 — Total interest paid: ₹96,67,200 − ₹50,00,000 = ₹46,67,200

This means for a ₹50 lakh loan at 7.5%, you end up paying over ₹47 lakhs (approx.) purely as interest over 20 years — an important eye opener for any borrower.

You can use the below link to calculate the EMI and the breakup of interest and principal using the link – EMI Calculator Online | Home, Personal, Business Loan & LAP – Borrowww

Factors That Affect EMI

The EMI is affected by several factors, the most important being the loan amount—a higher principal payment increases the monthly EMI amount, which helps in the reduction of the tenure of the loan. The shorter the loan tenure, the lower the interest rate to be paid to the bank. The second most important factor is rate of interest; even a change in 0.05% ROI makes thousands of rupees change in the monthly EMI for a substantial loan amount. Third is the tenure, which works inversely, i.e., the higher the tenure, the lower the EMI, and the lower the tenure, the higher the EMI.